| For individuals and companies earning income between India and the UAE, the India–UAE Double Taxation Avoidance Agreement (DTAA) plays a decisive role in determining where tax is payable. However, treaty benefits are not automatic. To formally claim reduced tax rates or exemptions under the DTAA, a UAE resident must provide official proof of tax residency — typically through a Tax Residency Certificate (TRC) issued in Dubai. |

Introduction

As cross-border trade, investment, and talent mobility between India and the UAE continue to expand, the India–UAE Double Taxation Avoidance Agreement (DTAA) has become one of the most frequently invoked bilateral tax treaties by Indian professionals, investors, and businesses operating from Dubai.

Yet one of the most common misunderstandings is that treaty benefits apply automatically the moment an individual or entity qualifies as a UAE resident. In reality, Indian tax law and the treaty framework both require formal documentary proof — and the Tax Residency Certificate (TRC) issued by the UAE Federal Tax Authority is the cornerstone of that proof.

This guide explains how a TRC enables DTAA claims, which income categories are most affected, and what Indian and UAE tax authorities expect in terms of documentation and compliance.

Why a TRC Is Mandatory for India–UAE DTAA Claims

Under Section 90 of the Indian Income Tax Act, a taxpayer claiming relief under a tax treaty must submit a Tax Residency Certificate from the contracting state where they are resident. This requirement is mandatory, not discretionary.

Without a valid TRC, the following consequences typically apply:

- Standard domestic Indian withholding tax rates apply instead of treaty-reduced rates

- Reduced withholding rates may be denied at source by Indian payers

- Treaty exemption claims may be rejected during assessment or scrutiny

- Indian tax filings as a non-resident may be challenged

This makes the TRC the foundational compliance document for anyone invoking the India–UAE treaty. No other document, including Emirates ID, UAE visa, or bank statements, substitutes for it in formal treaty proceedings.

Key DTAA Articles Where TRC Becomes Critical

The India–UAE DTAA allocates taxation rights across multiple categories of income. Below are the primary provisions where TRC submission becomes operationally important:

1. Dividend Income (Article 10)

Dividends paid by Indian companies to UAE resident shareholders may attract withholding tax in India. The treaty may cap the applicable withholding rate, but this reduced rate is available only upon TRC submission and beneficial ownership confirmation.

Indian companies routinely require the following before applying treaty rates:

- A valid UAE Tax Residency Certificate covering the relevant financial year

- Form 10F, as prescribed under Indian tax law

- A declaration of beneficial ownership

Without a TRC, dividend payments are typically taxed at full domestic rates, significantly increasing the tax cost for UAE-resident shareholders.

2. Interest Income (Article 11)

Interest earned on loans, bonds, fixed deposits, or other financial instruments sourced from India is subject to Indian withholding tax. The India–UAE DTAA prescribes a reduced rate for eligible UAE residents.

For UAE-resident lenders or investors holding Indian debt instruments, submitting a TRC ensures the treaty rate is applied at source rather than the higher domestic rate. Certain government-backed entities may qualify for additional exemptions under this article, subject to documentation.

3. Royalties and Technical Service Fees (Article 12)

Cross-border royalty payments, software licensing fees, and technical service charges between Indian and UAE entities represent a growing and commercially significant category.

India typically imposes withholding tax on such payments. Claiming treaty-reduced rates requires:

- A valid UAE TRC

- A beneficial ownership declaration

- Appropriate contractual documentation establishing the nature of services

For businesses engaged in intellectual property licensing, software exports, or consulting arrangements with Indian clients, this provision can materially affect net cash flows and project economics.

4. Business Profits (Article 7)

Under the India–UAE DTAA, the business profits of a UAE-resident enterprise are taxable only in the UAE unless the enterprise maintains a Permanent Establishment (PE) in India. This is one of the treaty’s most commercially valuable provisions for UAE-based service providers and consulting firms.

To assert this position effectively with Indian counterparties and tax authorities, a TRC helps establish:

- UAE tax residency of the enterprise

- Treaty entitlement to Article 7 protection

- Non-resident classification under Indian income tax law

In cross-border service contracts, especially where Indian clients are required to deduct tax at source, the TRC is often the document that determines whether withholding applies at all.

5. Capital Gains (Article 13)

Capital gains taxation under the India–UAE DTAA depends on several factors, including the nature of the asset, its location, and the type of entity involved. In certain situations, India retains taxing rights — for example, on gains from shares of Indian companies.

However, proper residency documentation remains essential to:

- Establish treaty status and access Article 13 provisions

- Avoid residential classification disputes with Indian authorities

- Support accurate non-resident tax filings in India

A TRC materially strengthens the treaty-based position in capital gains scenarios, particularly for UAE residents managing high-value Indian equity portfolios, real estate interests, or business exit transactions.

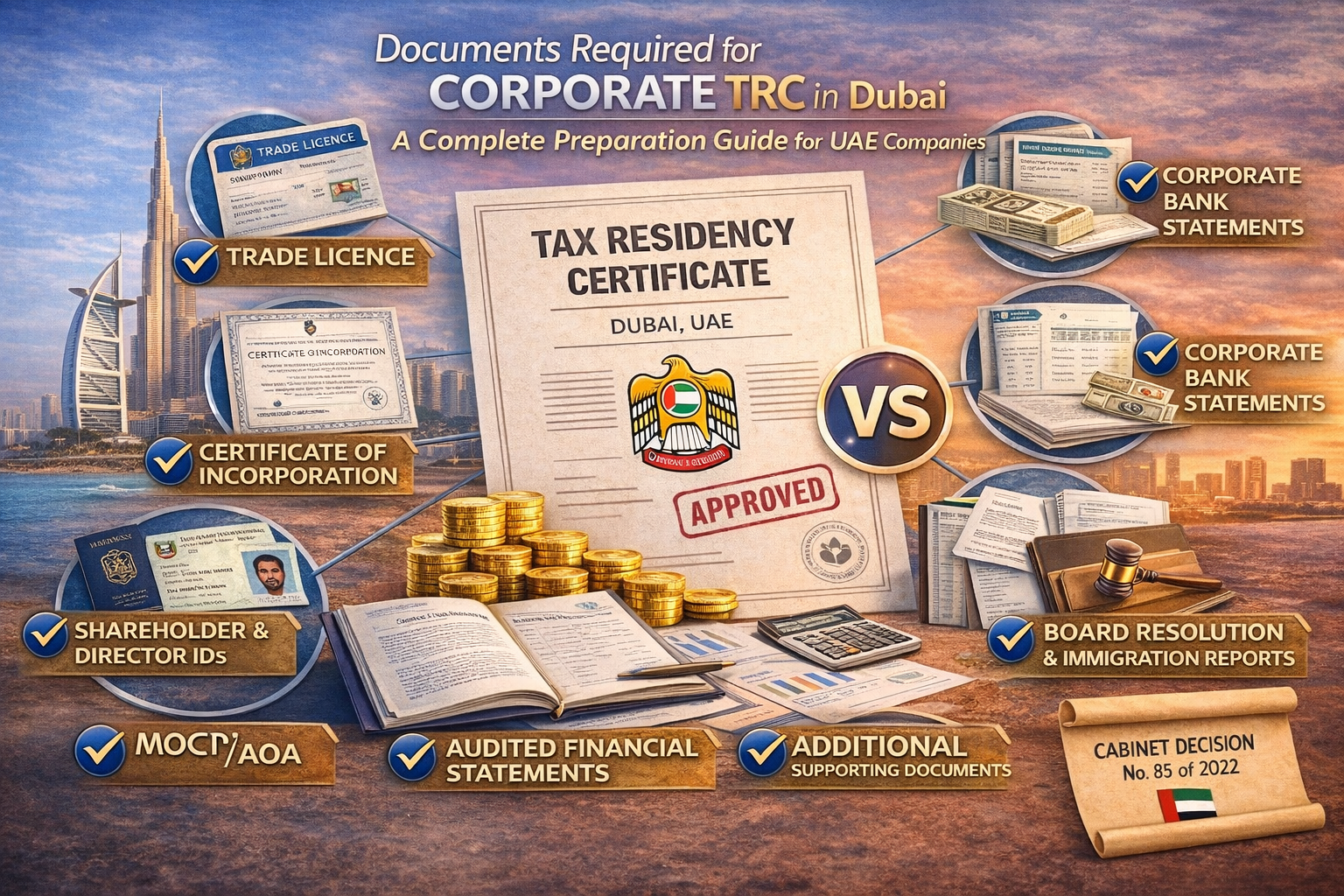

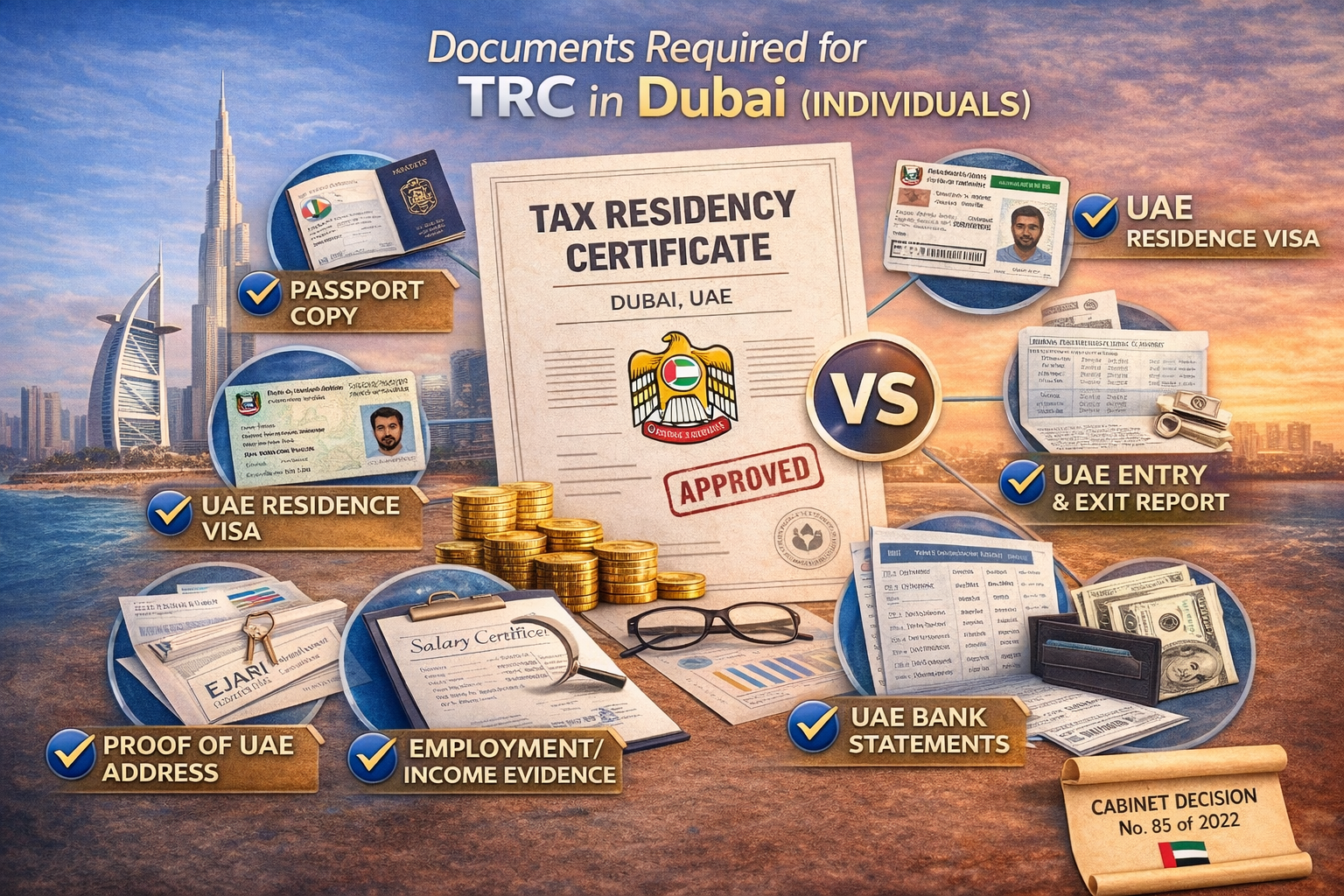

Corporate vs Individual DTAA Claims: Key Differences

Both individuals and companies can invoke India–UAE DTAA benefits, but the compliance pathways differ significantly.

Individual DTAA Claimants

Individuals typically seek treaty relief on:

- Salary income received from Indian employers

- Consulting or freelance income paid by Indian clients

- Investment income including dividends, interest, and capital gains

- Rental income from Indian properties

Corporate DTAA Claimants

Companies and business entities most commonly invoke treaty benefits for:

- Intercompany service payments and management fees

- Cross-border technical services and consulting contracts

- Royalty and intellectual property licensing arrangements

- Financing structures and cross-border lending

In corporate transactions, treaty rate application typically occurs at source — meaning Indian payers deduct withholding tax before remitting payment. TRC submission must therefore occur before payment processing to avoid the need for subsequent refund claims.

How Indian Tax Authorities Evaluate DTAA Claims

Indian tax authorities have become increasingly rigorous in evaluating treaty claims, particularly following the OECD’s Base Erosion and Profit Shifting (BEPS) initiatives. A TRC is necessary but not always sufficient on its own.

Key evaluation criteria include:

- A valid TRC covering the relevant Indian financial year (April to March)

- Beneficial ownership of the income being claimed under the treaty

- Economic substance of UAE residency, including physical presence, business activity, and decision-making

- Absence of treaty abuse or artificial arrangements

The India–UAE DTAA includes anti-abuse provisions aligned with international BEPS standards. Obtaining a TRC without genuine economic substance in the UAE may not guarantee treaty relief if the overall arrangement is challenged as lacking commercial reality.

TRC and Form 10F: The Required Compliance Combination

For claiming India–UAE DTAA benefits, a TRC alone is typically insufficient under Indian law. Indian regulations additionally require the submission of Form 10F, which captures:

- The taxpayer’s nationality

- Tax identification number in the country of residency

- The period of residency covered

- The address in the country of residency during the relevant period

Since 2022, Form 10F must be filed electronically on India’s income tax portal. Failure to file Form 10F electronically can invalidate treaty claims even where a valid TRC exists. Both documents must be in order before treaty rates are applied or before Indian tax filings are made.

Common DTAA Claim Scenarios Requiring a TRC

The following are the most frequently encountered situations where a TRC is required for India–UAE DTAA claims:

- Receiving dividend income from Indian public or private companies

- Providing advisory, consulting, or professional services to Indian clients

- Licensing software, patents, or other intellectual property into India

- Earning interest income from Indian loans, bonds, or fixed deposits

- Structuring cross-border business contracts with Indian counterparties

- Filing Indian income tax returns as a non-resident claiming treaty relief

- Managing high-value Indian equity or mutual fund portfolios from Dubai

In each of these situations, treaty rates and benefits apply only with proper and timely documentation. Retroactive treaty claims are possible but involve refund filings, longer processing timelines, and increased audit risk.

Practical Illustration

Consider a Dubai-based consultancy firm that provides strategic advisory services to an Indian corporate client. Under the service agreement, the Indian company is required to deduct withholding tax at source.

| Without treaty documentation: Withholding is applied at the standard domestic Indian rate (typically 10–20% depending on the service category), significantly reducing the net amount remitted to the UAE firm.With TRC + Form 10F submitted before payment: The applicable DTAA rate is applied, reducing withholding tax, improving cash flow, and eliminating the need for refund filings. Across multiple contracts over a financial year, the financial impact can be substantial. |

Anti-Abuse and Economic Substance Considerations

Modern treaty interpretation has evolved significantly. Indian tax authorities, guided by BEPS Action Plans and domestic General Anti-Avoidance Rules (GAAR), evaluate whether treaty claims reflect genuine economic arrangements.

Key concepts that influence treaty claim evaluation include:

- Principal Purpose Test (PPT): If one of the principal purposes of an arrangement is to obtain treaty benefits, relief may be denied

- Beneficial ownership: Income must be genuinely owned by the UAE resident, not held as an agent or conduit

- Substance-over-form analysis: UAE residency must reflect real commercial activity, not merely a tax-motivated relocation

A TRC should therefore form part of a broader, compliant cross-border structure — not a standalone tactic. Taxpayers with genuine UAE residence, substantive business operations, and defensible commercial arrangements are best positioned to benefit from treaty provisions.

Why Timely TRC Application Matters

A critical and frequently overlooked requirement is that the TRC must be valid at the time of income receipt and, ideally, submitted before withholding occurs. Specifically:

- The TRC must cover the relevant Indian financial year (April to March)

- It must be valid at the time the income is received or the transaction is completed

- Indian payers typically require TRC submission before processing payments at treaty rates

Applying for a TRC after tax has already been deducted at the domestic rate requires filing a refund claim in India, which involves additional time, administrative effort, and scrutiny risk. Proactive documentation significantly reduces compliance burden and improves cash flow certainty.

Strategic Importance for High-Value Transactions

For high-net-worth individuals (HNIs), family offices, and businesses engaged in significant cross-border India–UAE transactions, TRC-backed treaty planning offers material financial advantages:

- Reduced withholding tax on investment income improves net returns

- Treaty-based protection for business profits minimises Indian tax exposure on service income

- Clear allocation of taxing rights reduces the risk of double taxation on the same income

- Well-documented treaty positions are more defensible during scrutiny or assessment

- Consistent compliance establishes credibility with Indian tax authorities over time

For businesses planning major exit events, block transactions, or restructuring involving Indian assets, coordinating TRC timing with transaction execution is particularly important.

Conclusion

Claiming benefits under the India–UAE Double Taxation Avoidance Agreement requires more than treaty eligibility — it requires formal, documented proof of UAE tax residency, submitted at the right time and in the correct format.

A Tax Residency Certificate issued in Dubai serves as the primary document enabling:

- Reduced withholding tax rates on dividends, interest, royalties, and service fees

- Treaty-based exemptions for qualifying business profits

- Clear allocation of taxing rights between India and the UAE

- Stronger compliance positioning in assessments and scrutiny

For individuals and businesses engaged in cross-border India–UAE transactions, obtaining a TRC is not optional when invoking treaty relief — it is foundational. Combined with Form 10F, beneficial ownership documentation, and genuine UAE residency, a TRC forms the backbone of an effective India–UAE tax compliance strategy.